This blog series is given in four parts.

See parts: One | Two | Three | Four

Welcome to part two of our blog series on the impact of the digital twin concept. In the previous article, we delved into the early stages of stamped parts and assemblies. Now, we turn our attention to the crucial aspects of planning and budgeting.

While process planning and cost evaluation have traditionally relied on historical data and manual estimations, the advent of digital twin technology has revolutionized this field. By leveraging 3D models and comprehensive data, modern systems offer precise assessments, enabling accurate budgeting and efficient resource allocation. However, implementing this technology brings its own set of challenges, from training personnel to integrating process planning with tooling design.

In this article, we explore the benefits, complexities, and management considerations associated with using the digital twin for planning and budgeting. So, let’s delve into the exciting intersection of virtual simulations and real-world estimations to discover the potential gains in costs and deadlines that await us.

Planning and budgeting:

The task of process planning and cost evaluation of stamped parts and assemblies is already usually assigned to personnel with knowledge and some experience in stamping and assembly processes, who are reasonably familiar with the details of each one and can identify what will be required during production. It is also very common to use previous tooling construction and manufacturing history to perform cost estimates, including the use of customized spreadsheets and dedicated computer programs.

However, usually evaluations based on historical data only consider the type of part, its size, material employed, etc., but do not take in account more specific aspects concerning the geometry and other actual features of each component or assembly. This way, in many cases important details that will impact tooling and production costs end up not being considered. There are also situations where new parts have innovative designs or materials that are not similar to those that have been implemented before (something common at a time of drastic changes in the market, such as now with the broad electrification of the automotive industry).

In these cases, the application of the Digital Twin becomes an important tool that allows to guarantee the assertiveness of the estimates in an objective way, based on the real characteristics of each new part from its 3D models and full data. The modern systems available for this application use technologies that enable the automatic identification of the main features of each component and the definition of specific processes for its manufacture, going all the way to the estimation of material consumption for the construction of tools, the generation of the tooling parts list and the estimate of lead times for the needed tasks. This allows not only budgeting the tools themselves, but also estimating the workload of the tooling shops and planning the distribution of tasks to be performed among available suppliers, with large potential gains in costs and deadlines.

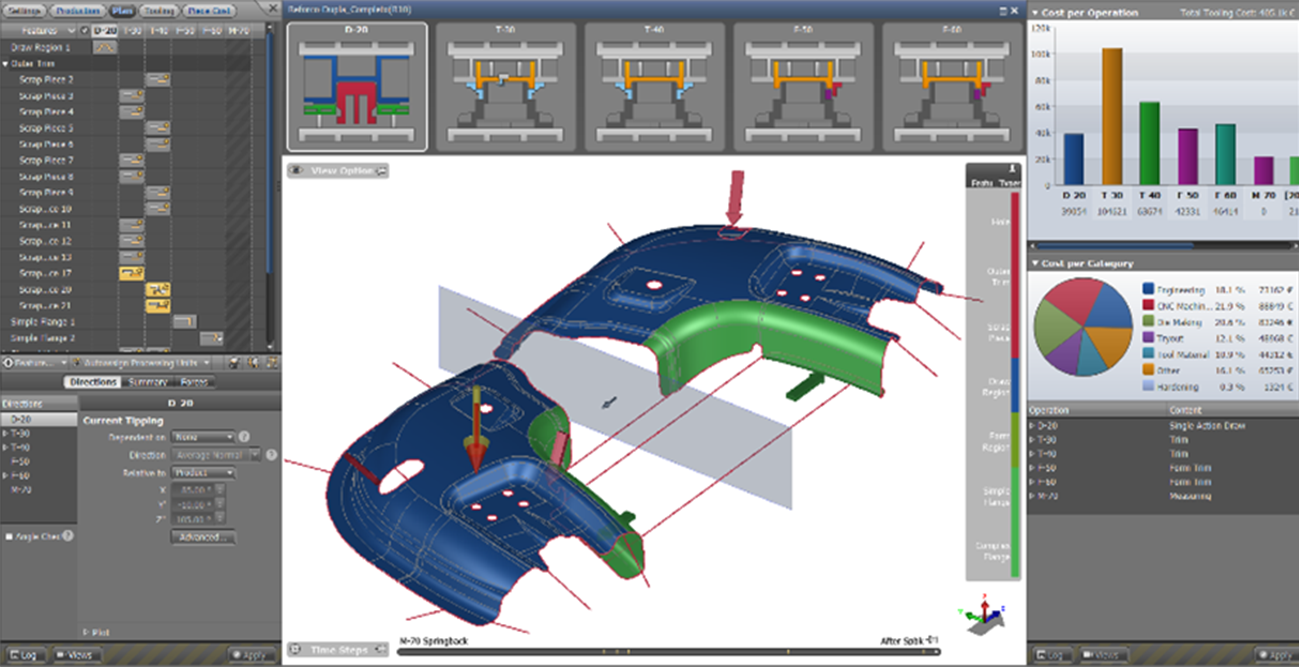

The implementation of this kind of technology, on the other hand, also faces difficulties at the management level. First, it is usual that the technical personnel engaged in the planning of the forming and assembly processes of sheet metal parts do not have a more considerable experience with advanced systems that employ 3D modeling and are basically users of numerical tables. It is not always easy or even possible to train these personnel to use the Digital Twin, which starts from part’s 3D geometric models to execute estimates of deadlines, material usage, etc., as can be seen in the example of the Figure 1. Managers need to be aware of this kind of difficulty, which in some cases can make it necessary to transfer personnel from other departments such as Manufacturing Engineering or Tool Design, to add them to the budgeting team.

Fig. 1: Example of a planning and budgeting system that is based on 3D geometry of the parts.

Another aspect that the management must be aware of is the interaction between process planning and the design of the tooling itself. Construction, assembly, and operation details of the tools may require process changes that impact the deadlines and costs defined in the planning stage. Managers are responsible for ensuring that there is an effective integration between both activities (which in many cases may even be being developed in different companies, since it is common to subcontract tooling projects) so that cost reduction potentials can be availed or any cost and schedule increases that may be necessary are analyzed and incorporated into the planning.

?")

{kind=link}